What is apartment syndication? This becomes a far more practical question once you move past definitions and start understanding how capital, decision-making, and execution come together inside a real deal.

Most explanations stop at a surface-level description of pooling money to buy a property, which leaves out the part that actually matters. Structure, alignment, and execution determine outcomes, and those elements rarely show up in basic overviews.

Investors who approach apartment syndication with a clear understanding of how the model functions tend to ask better questions, evaluate opportunities more effectively, and recognize how operator decisions shape the trajectory of a deal.

What Apartment Syndication Means in Practice

Apartment syndication allows a group of investors to collectively acquire a multifamily property through a structured partnership. One group, often called the sponsor or operator, identifies the opportunity, structures the deal, and manages the business plan. Another group, the investors, contributes capital and participates in ownership.

A syndication creates access to larger properties that individual investors would not typically acquire on their own. According to National Multifamily Housing Council, over 40 million Americans live in apartment housing, which reflects the scale and demand behind multifamily as an asset class.

That demand underpins why syndication has become a common structure for acquiring and operating these properties.

The Structure Behind a Syndication

A typical apartment syndication organizes ownership through a legal entity, often a limited liability company. The sponsor manages the entity and oversees the property, while investors hold membership interests.

Key roles inside the structure

- Sponsor or Operator

The sponsor sources the deal, arranges financing, executes the business plan, and manages the property through its lifecycle. - Investors

Investors contribute capital and receive a share of ownership based on their investment. - Property Management Team

A professional management company handles day-to-day operations, including leasing, maintenance, and resident communication.

This structure allows each participant to focus on a specific role, which creates efficiency when executed properly.

GP vs LP: Where Investors Sit in the Capital Stack

Understanding the difference between a General Partner and a Limited Partner clarifies how responsibility, control, and capital flow through a syndication.

General Partner (GP)

The General Partner operates the deal.

This group includes the sponsor and operating team responsible for:

- Sourcing and acquiring the property

- Securing financing

- Executing the business plan

- Making day-to-day and strategic decisions

- Communicating with investors

The GP carries decision-making authority and operational responsibility throughout the life of the investment.

Limited Partner (LP)

The Limited Partner provides capital and participates in ownership.

LP investors typically:

- Contribute equity to the deal

- Receive a proportional ownership interest

- Do not participate in daily operations

- Rely on the GP to execute the business plan

Most passive investors in apartment syndications participate as Limited Partners.

Where LPs Sit in the Capital Stack

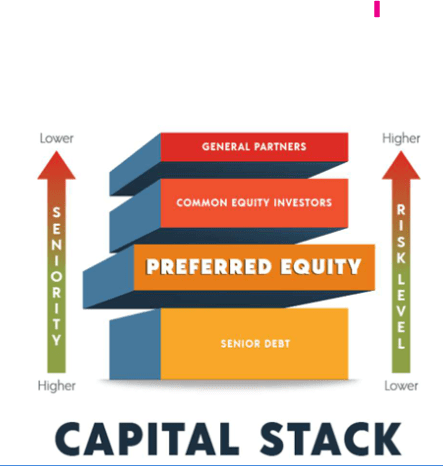

The capital stack represents how a property gets financed, and where different participants sit in terms of priority and structure.

In a typical multifamily syndication:

- Debt sits at the top

A lender provides a loan secured by the property and holds first claim on the asset. - Equity sits below debt

This equity comes from both the GP and LP investors.

LP investors sit within the equity portion of the capital stack. Their position reflects ownership in the deal rather than a lending role. The GP often invests alongside LPs, which aligns interests across the partnership.

This structure means:

- Debt holders receive priority based on loan terms

- Equity participants, including LPs and GPs, participate in ownership and outcomes tied to the property

Understanding where you sit in the capital stack helps frame expectations around how the investment functions within the overall structure.

How a Deal Comes Together

Apartment syndications follow a sequence that starts well before investors see an opportunity and continues long after closing.

- Sourcing the Opportunity

Operators review markets, properties, and financials to identify assets that align with their strategy.

- Underwriting and Due Diligence

The team evaluates income, expenses, physical condition, and market dynamics to determine whether the deal fits their criteria.

- Structuring the Investment

The sponsor defines how the partnership will function, including capital requirements, ownership structure, and governance.

- Raising Capital

Investors review the opportunity and decide whether to participate based on their own criteria and understanding of the deal.

- Closing and Execution

After closing, the operator implements the business plan, which may include renovations, operational improvements, or repositioning.

- Ongoing Management

The property operates over a defined hold period, during which the sponsor manages performance and communicates with investors.

- Exit

The deal concludes through a sale or refinance, depending on market conditions and strategy.

Each stage requires coordination, discipline, and consistent decision-making.

What Happens After You Invest

Many investors focus heavily on the acquisition phase, yet the majority of the investment lifecycle unfolds after the deal closes. The underwriting, the projections, and the business plan set the direction, but the actual outcome is determined over the years that follow.

Once invested, the role of the investor shifts. Control largely transfers to the sponsor, and the experience becomes one of monitoring rather than managing. Communication becomes the primary connection point. Sponsors typically provide regular updates, financial reports, and commentary on performance, offering insight into how the property is tracking relative to initial expectations. The quality, transparency, and consistency of this communication can vary, which is why sponsor selection is often as important as deal selection.

Operational execution is what ultimately drives results during this period. Leasing performance determines revenue stability and growth. Expense management, particularly in areas like insurance, taxes, payroll, and maintenance, directly impacts net operating income. Capital improvements must be executed on time and within budget to achieve projected rent premiums. Each of these variables introduces a layer of execution risk, even when the initial strategy is sound.

External factors continue to influence performance as well. Market rent growth may slow or reverse. Supply pipelines can create unexpected competition. Interest rate environments can impact refinancing options and exit timing. These forces are outside of the sponsor’s control, yet they shape the trajectory of the investment in meaningful ways.

Liquidity is another important consideration. Unlike publicly traded investments, capital is typically locked up for the duration of the hold period, which may span several years. Investors generally do not have the ability to exit early without sponsor approval, and there may be limited or no secondary market for their ownership interest. This makes the initial decision to invest less about short-term performance and more about alignment with a longer-term strategy.

Cash flow expectations may also evolve over time. Distributions are often projected but not guaranteed, and they depend on actual property performance. In some cases, distributions may be reduced or paused to preserve capital, fund operations, or navigate challenging market conditions. In more stressed scenarios, additional capital may be required to support the asset, reinforcing the importance of understanding capital call risk before investing.

Ultimately, the post-acquisition phase is where the investment thesis is tested. It requires patience, a tolerance for variability, and confidence in the sponsor’s ability to adapt to changing conditions. Investors who approach this phase with a clear understanding of both the opportunities and the challenges tend to have a more realistic and informed investment experience.

The lifecycle of a syndication spans multiple years, which reinforces the importance of understanding how decisions compound over time rather than focusing only on the initial investment.

How Investors Evaluate a Syndication

Investors who approach syndications with a framework tend to navigate opportunities with more clarity.

- Sponsor Track Record and Approach Experience matters, yet understanding how a sponsor makes decisions often matters more. Investors should evaluate how the team has navigated different market conditions and how they communicate during periods of change.

- Market Selection Location influences demand, rent dynamics, and long-term viability. Data from CBRE highlights that population growth and employment trends continue to shape multifamily performance across major U.S. markets.

- Business Plan A clear plan outlines how the operator intends to manage and improve the asset. Investors benefit from understanding the assumptions behind that plan rather than relying on high-level summaries.

- Alignment of Interests The structure should align the sponsor and investors in a way that reflects shared incentives over the life of the deal. Evaluation does not require predicting outcomes. It requires understanding how the pieces fit together.

Where Syndications Can Become Challenging

Apartment syndication involves multiple moving parts, and not every investment unfolds according to the original underwriting. Market conditions shift, sometimes quickly. Interest rates can rise, compressing cash flow and limiting refinance options. Operating expenses such as insurance, taxes, and payroll can increase beyond projections. Even well-planned execution can encounter delays or underperformance, whether due to leasing velocity, renovation timelines, or broader economic pressure.

In this context, capital calls become an important concept to understand upfront. A capital call is a request from the sponsor for investors to contribute additional funds beyond their initial investment, typically used to address operating shortfalls, fund unexpected expenses, or support the business plan during periods of stress. While not every deal will require one, they are a structural reality in private real estate investing, particularly when external conditions move against the original assumptions.

The challenge is not simply that additional capital may be required, but that the timing and necessity of a capital call are often unpredictable. Investors may be asked to deploy more capital during less favorable market conditions, and those who choose not or are unable to participate may face dilution of their ownership or changes to their position within the investment. At the same time, sponsors must balance preserving the asset with protecting investor capital, which can lead to difficult decisions under pressure.

Understanding these dynamics in advance creates a more grounded perspective on how multifamily investments operate. Rather than viewing projections as fixed outcomes, experienced investors recognize that these investments exist within broader economic cycles and require adaptability from both sponsors and limited partners. A clear awareness of potential challenges, including capital calls, allows investors to evaluate opportunities with a more informed and realistic mindset.

Why Syndication Exists

Syndication exists because it solves a scale problem.

Larger multifamily properties require significant capital, operational expertise, and ongoing management. A single investor rarely brings all of those elements together alone.

By combining capital and expertise, syndication creates a structure that allows properties to operate at scale while distributing ownership across multiple participants.

This model has supported the growth of institutional and private multifamily investment across the United States.

How Apartment Syndication Compares to Direct Ownership

Direct ownership places responsibility for acquisition, financing, and management on a single individual or small group. That approach provides full control but also requires full involvement.

Syndication distributes responsibility across a team. Investors participate in ownership while the sponsor manages execution.

Choosing between these approaches depends on how an individual wants to engage with real estate, not on a universal preference for one structure over another.

Apartment Syndication – a Structured Partnership

Apartment syndication becomes clearer when viewed as a structured partnership that combines capital, expertise, and execution over time.

Understanding how the model operates allows investors to move beyond surface-level explanations and engage with opportunities in a more informed way. The details behind structure, decision-making, and management shape the experience far more than simplified definitions.